How to Buy Mortgage Notes in 2026 [5 Steps]

Real estate notes are the most popular notes for investing.

This guide to buying mortgage notes is a comprehensive resource designed to help investors navigate the note-buying process.

We refresh the guide regularly as we field questions from our subscribers, interview experts, and evolve with the world of real estate note investing.

Bookmark this page and check back often to stay up-to-date.

Jump to:

What are Mortgage Notes?

Why Invest in Mortgage Notes?

How to Buy Mortgage Notes

Note Investing Success

Learn the differences between:

Mortgages and Notes

Notes and REO

Real Estate Investing and Note Investing

What are Mortgage Notes?

Definition of a Mortgage Note

A mortgage note is a borrower’s written promise to maintain lender repayment terms. Also known as a promissory note or real estate notes, mortgage notes are legal documents, though lenders don’t usually file them as public records.

The Different Types of Mortgage Notes

A mortgage promissory note is categorized by loan type, loan provider, lien position, performance, and asset class. Knowing the differences helps when it’s time to buy loan notes.

LOAN TYPE

Secured

When a tangible asset, like a property or a vehicle, is tied to a lien, it’s called a secured loan. A lender typically offers better interest rates and increased spending limits on secured loans since they have legal rights to sell the asset if the borrower defaults on the note.

Unsecured

When a lender issues a loan without a tangible asset and bases approval on a borrower’s credit history alone, it’s called an unsecured or signature loan. Unsecured loan interest rates are higher, and credit score requirements are more rigid than asset-backed secured loans.

LOAN PROVIDER

Private

Loans issued by private organizations or individuals are called private loans or private money. A private money loan doesn’t always follow traditional lending guidelines and offers borrowers flexibility in some cases. Investors may find private lenders with notes to sell, though the buying opportunities are usually limited to one per private seller.

Institutional

Loans issued by credit unions, banks, and other organizations in the loan-writing business are called institutional loans. Institutional lenders follow strict guidelines with minimal flexibility but issue a lot of loans. Note investors buying notes direct from institutional lenders benefit from recurring note availability, as opposed to the one-time private seller scenario.

LIEN POSITION

Lien position, aka lien priority or lien seniority, is the order in which the debt is paid in the case of default.

Debtors place liens (legal claims) on property to secure re-payment. Lien positions are established by order of recorded filing date. Usually, the mortgage lender holds the first priority, and other liens tied to the property hold junior positions.

Typically investors focus their investing either on first position or else on junior liens commonly referred to as seconds.

What Happens to Lien Positions During Foreclosure

If a foreclosure happens, the more senior the lien (first position), the more likely you are to be paid off and recover your investment because liens are paid off in order.

The trade-off in note investing is that while you pay much less for junior liens (often pennies on the dollar), you don’t enjoy the same security as senior lien investors or investors in the first lien position.

ASSET CLASS

Real estate asset classes categorize property types with similar attributes. Note investors can buy a broad range of notes across asset classes, including:

- Commercial

- Multifamily

- Residential

- Construction

When you’re starting out in mortgage note investing, the safest play is to invest in asset classes with which you are already familiar.

LOAN PERFORMANCE

A note buyer, in addition to understanding lien position and asset classes, needs to evaluate loan performance. Loans may be classified as non-performing, under-performing, performing, and re-performing.

- Non-performing note: A note that is 90 days or more past due.

- Under-performing note: Borrower has a history of being periodically late with payments.

- Performing note: A note being repaid on time and according to terms. Investing in performing notes is sometimes referred to as “clipping coupons” because the investor typically enjoys cash flow and modest returns paid back at regular intervals.

- Re-performing note: Borrower had missed payments, perhaps even went non-performing, but is now back on track. Sometimes these loans have been modified either by extended amortization, principal reduction, or interest rate reductions. One strategy note investors employ is to buy a non-performing loan and get it re-performing and then sell it as a re-performing note after seasoning (a period of on-time payments).

The biggest discounts for note investors usually come from non-performing notes, which are attractive to note buyers for the steep discounts and multiple exit strategies. Performing notes are the most secure and offer the note investor reliable monthly payments backed (collateralized) by real property.

What is the Difference Between a Mortgage and a Note?

A note refers to the promissory note, which is a signed agreement for the repayment of a loan.

A mortgage or a deed of trust is a legal instrument that pledges the real estate as collateral. The document also spells out how the lender can recover their investment if the promissory note terms aren’t met, typically by foreclosing on the real estate.

What is the Difference between a Note and REO?

In the banking industry, REO means “Real Estate Owned” and is short for “OREO,” an acronym for “Other Real Estate Owned.” Lenders use the term as a line item on reports to track real estate acquired through the foreclosure process.

When a lender owns a note (a loan) on a property, they retain the paper or document and the rights and responsibilities it outlines.

When a borrower fails to pay for an extended period, the loan becomes “non-performing.” The lender may choose to exercise its right to foreclose on the property to recoup the lender’s investment.

When a lender forecloses on a property, the lender gains the right to sell the property at a foreclosure sale. However, until the selling process is complete, the borrower retains ownership of the property, while the bank owns the non-performing note.

At the foreclosure sale, the lender may exercise its right to bid. Since the lender already has a mortgage note on the property, the bid isn’t made with new money, but rather, the lender makes what’s called a credit bid.

The lender can bid a maximum of the total amount owed on the property, including the unpaid principal balance (UPB) plus any default interest and foreclosure costs, up to the amount that makes the lender “whole,” meaning they have recovered all of what they’ve invested and any additional interest and penalties accrued.

The lender is not required to make the maximum bid, or any offer for that matter, as long as the foreclosure sale is defensible as commercially reasonable (another topic for another day) or, in other words, fair.

If the lender’s credit bid is the highest at the auction, the lender repossesses the property at the foreclosure sale. At this point, the loan is extinguished, and now the lender owns the real estate. Lenders then log the real estate as OREO, or as it’s commonly called, REO.

What is the Difference between Real Estate Investing and Note Investing?

When investing in notes, you’re buying the debt secured by a piece of property, the promise of repayment, and (generally) the right to foreclose and recoup your investment if the borrower fails to meet obligations or make payments. You just don’t own the physical real estate.

Real estate investors gain full access to a property when they purchase it. A note owner doesn’t have the rights to use or enter the property unless outlined in the loan agreement.

When you own a real estate note, the payments you receive are fixed according to the note. Vacancies, rent collection, or market forces should not impact what’s owed.

Under normal circumstances, as the note investor, you are not responsible for collecting rent or dealing with “tenants, toilets, and trash.”

Real estate investors are impacted when a property’s value goes down, tenants don’t pay, or capital improvements are required. Note investing mitigates property-related losses.

On the flip side, mortgage loan investors don’t benefit from property appreciation. As a note investor, you trade the potential speculative appreciation for set payments with a defined schedule, interest rate, and term.

When you invest in real estate, you have the right to undisturbed use of the property. If you’ve leased the property, you have the right to collect rents while your tenant has the right to “quiet enjoyment.”

If you’ve borrowed money to buy the property, then in addition to your rights of use, you have obligations to pay your loan and maintain the property to prevent it from falling into disrepair.

As a real estate investor, you enjoy both the rewards of appreciation as well as the risks of price correction. If the property’s value goes up, all of the appreciation goes to the property owner, not the lender.

If the property’s value goes down, the note is unaffected, the amount owed stays the same, and the same payments must be made regardless of occupancy, rent collection, and market forces.

Why Invest in Mortgage Notes?

Purchasing mortgage notes can be an excellent investment for someone looking for passive income secured by real estate. As with any investment, you should fully understand what you’re buying before you dive in.

Regular Monthly Income

When you buy a note, you become the bank. Buy a performing note, and you can expect payment on time by a credit-worthy borrower. You’ll get some of your money out plus a little bit of interest, and it’s all secured by that real estate, making it an attractive way to invest in performing notes.

Capital Stack Security

The various levels of financial sources funding a property build the capital stack. Equity is at the top, homeowner association (HOA) and maintenance fees are at the bottom, and first and second mortgages rank in priority between them.

When real estate prices correct and come down, the equity gets cut out first. Mortgage holders maintain their position within the asset, but mortgage note investors aren’t impacted in this scenario. Note investors won’t enjoy potential appreciation benefits, but the note investment remains secure.

EXAMPLE OF CAPITAL STACK LOSS:

Property Investment: $100,000

Money Down: $20,000

Mortgage Balance: $80,000

Property Value After Market Correction: $70,000

What Happened?

The property owner lost $20,000 and is now deeper in debt by $10,000, called a deficiency. The lender hasn’t lost anything but retains foreclosure rights on the property. However, to recoup the deficiency, a lender may wait until the market works in its favor.

Other factors to consider when evaluating whether buying a specific mortgage note is a good investment include:

- The Seller Sadly, there has been a scourge of hucksters and fly-by-nights who have sold a variety of bad assets with false promises. Make sure you’re dealing with a trustworthy seller.

- The Property Since the property is the collateral for the note you’re buying, you must have a reasonable understanding of the property’s value and the prospects of future value.

- The Borrower Although as a note investor, you have remedies for non-paying borrowers if your investment is concentrated in a single asset, you need to have reasonable assurance that the borrower is unlikely to damage or destroy your collateral.

- The Market Since the market, including the foreclosure laws and timelines for the municipality, may impact the value of the collateral or the costs to recoup your investment in the event of non-payment, you should be comfortable with and understand the market where your collateral sits.

With properly aligned goals, education, and expectations, buying mortgage notes can be a great investment.

How Do Mortgage Notes Make Money?

Making money on a real estate note investment depends on the type of notes you buy and the acquisition strategy.

HOW DO PERFORMING NOTES MAKE MONEY?

If you buy a performing real estate note, you receive payments according to the payment schedule, term, and interest rate. You accept those payments while enjoying the security of having your payments backed by the real estate.

HOW DO NON-PERFORMING NOTES MAKE MONEY?

There are other ways to make money with real estate notes. Note investors buying non-performing notes employ a variety of advanced strategies, including:

- Loan to Own Some investors will buy a non-performing note to exercise power to foreclose and take possession of the real estate.

- Loan Modifications Private investors often have more flexibility than institutional lenders in the options they can offer delinquent borrowers. Some investors buy a non-performing note at a discount to provide more favorable repayment terms to the borrower. The note is then re-established as performing, and the investor enjoys regular payments.

- Selling Partials The note investor sells payment portions to a third party for a margin above what was originally paid.

- Selling Re-Performers The note investor buys the non-performing note at a discount off the unpaid principal balance (UPB). Next, the investor works with the borrower to get the loan re-performing, and finally, the investor sells the now re-performing note to another investor at a markup.

- Flipping or Brokering Notes The highest value task in the note investing business is finding the note. You can profit from flipping notes, even if you don’t have money of your own, by finding real estate notes for investors who have the capital.

- Foreclosure It’s true. I had a client who bought a commercial property note for a pretty steep discount. Since the original lender, a community bank, had already begun the foreclosure proceedings, my investor client assumed the role of the foreclosing lender and hired us to market the asset for a foreclosure sale. The result was a profit of well over $300,000 in a matter of weeks, having sold the property at the foreclosure sale to a third party. My client never got in the chain of title and only owned the paper for about six weeks from start to finish.

I’m sure we’ll hear from seasoned investors about additional ways to make money with real estate notes. If that’s you, let us know in the comments below.

What is the Risk of Investing in Mortgage Notes?

Real estate note investing, when done right, should be LESS RISKY than real estate investing. Just as investing in bonds is considered safer than equities or stocks, the same is true for investing in real estate notes vs. investing in real estate.

As a note investor, you are trading the upside potential of appreciation in exchange for limiting the downside risk. This isn’t to say that there is “risk.”

The amount of risk in a note investment depends on the loan underwriting, the Loan to Value (LTV), the position (senior, junior) of the debt, the good faith of the borrower to some degree, the locale’s regulatory environment, and the quality of the documents, assignments, and allonges.

There is, of course, always risk in any investment, and as an investor, it is up to you to evaluate the risk for any investment you make.

How to Buy Mortgage Notes

When it comes to buying mortgage notes, there aren’t a lot of hard-and-fast rules about the process and how it’s done. In fact, you can even buy notes with no money.

Buying a home is very standardized, while buying notes is reserved for investors. Standard real estate transaction procedures and regulations don’t apply when buying the real estate’s mortgage note.

A transaction’s participants largely determine the note-buying

process, so details will vary with each purchase. In the end, you need documents that transfer lender rights to you.

Ready to begin on the path to note ownership? Use our simple, 5-step process. You’ll be buying mortgage notes in no time.

Step 1: Find Real Estate Notes to Buy

Finding real estate notes is easier when you know where to look. Your business strategy and experience determines where you should buy notes. Investors can buy mortgage notes online, build a lender network, or acquire notes from multiple sources, including:

- Private note holders, usually seller-financed property or business sales

- Hedge or private equity funds that buy in bulk from banks and servicers and then resell

- Note exchanges and marketplaces

- Special servicers

- Banks and credit unions

Step 2: Note Tapes

A “tape” is simply a spreadsheet with a note’s loan numbers and other relevant information.

Once you’ve received a tape, you’ll have the note details you need to start the due diligence process.

Step 3: Note Buying Due Diligence

Mortgage note due diligence processes closely correlate with the note buying strategy you’re pursuing. In all cases, you’ll want to see a title report.

Buying a multi-million dollar “loan to own” single, small-balance commercial note on which you intend to promptly foreclose requires a very different due diligence process than 100 non-performing junior liens that you’re buying for six cents on the dollar and plan to “rehab” and modify.

Want to shortcut the note due diligence? Contact our expert residential note evaluations partner, Craig Everett, who will do it for you. You’re welcome.

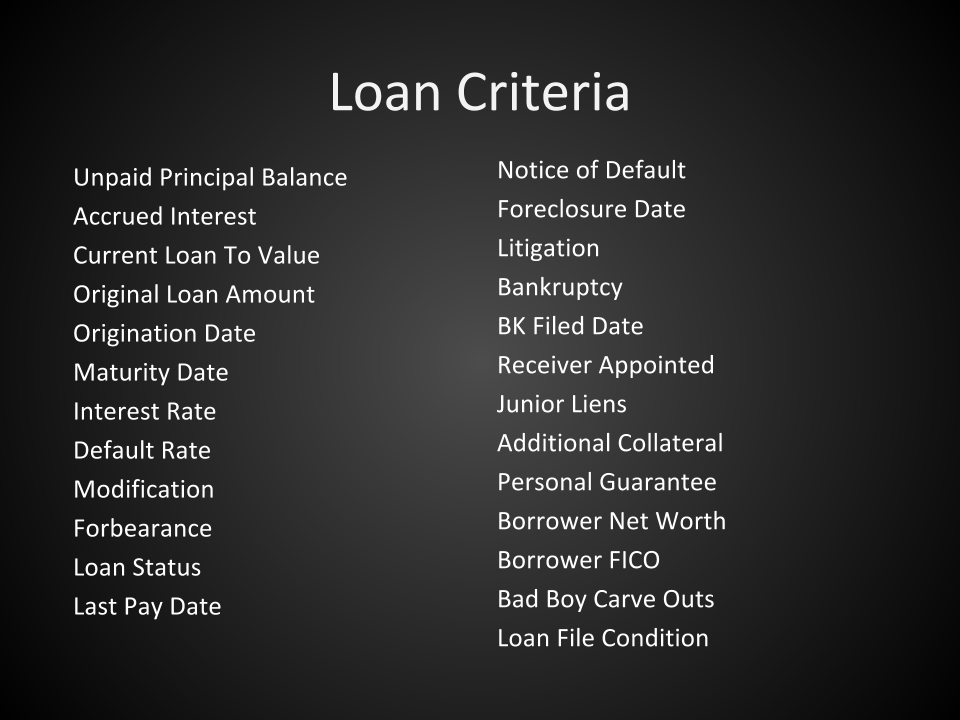

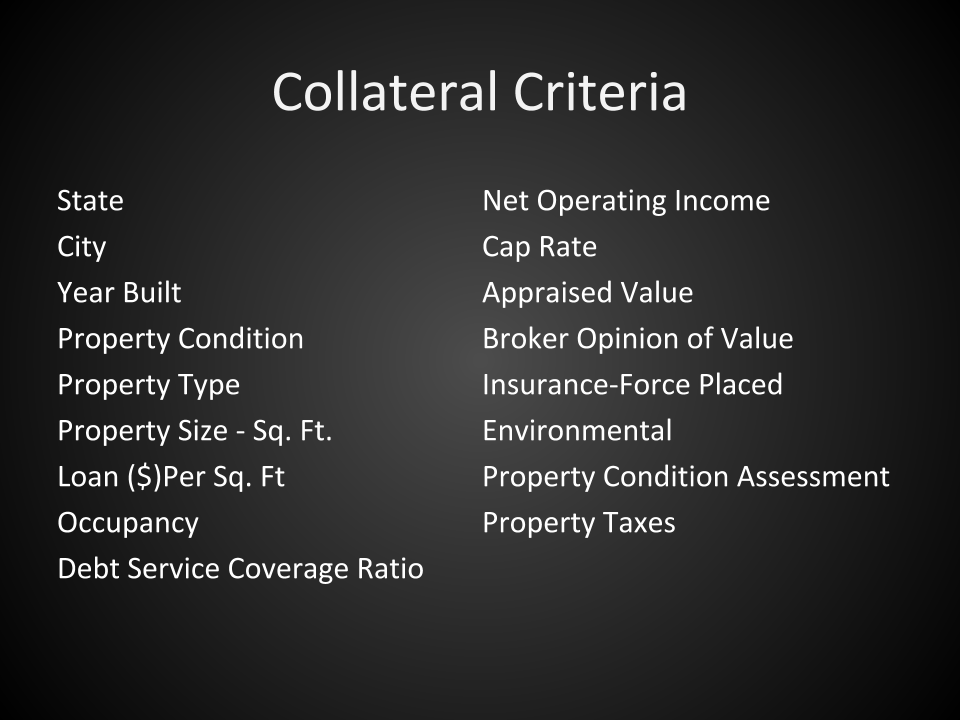

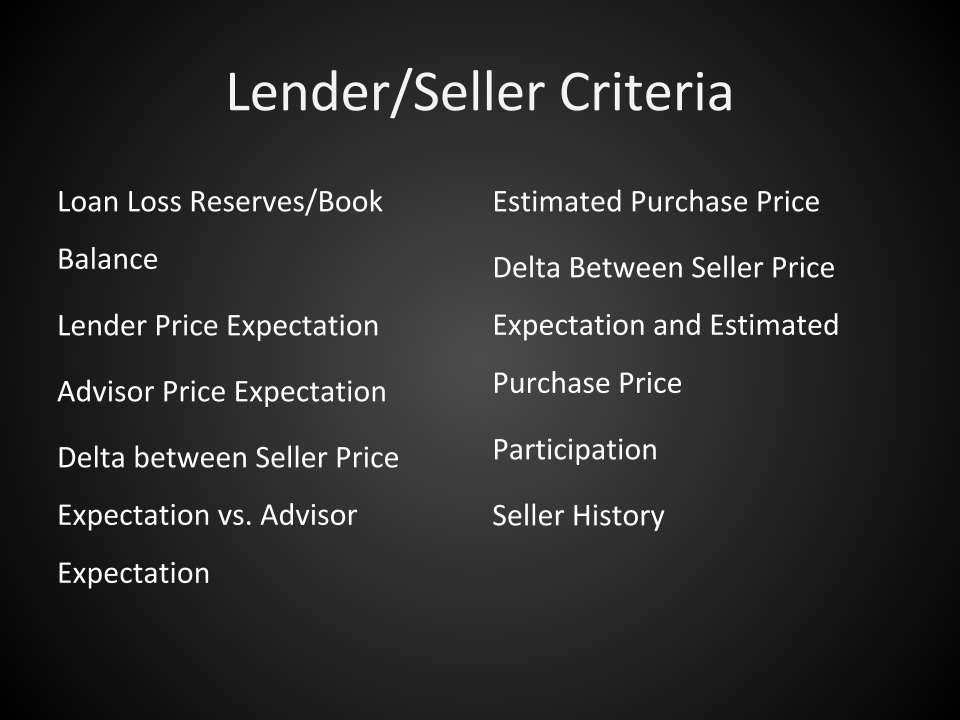

EVALUATING NOTES WITH LASER: LOAN ACQUISITION SUITABILITY AND EVALUATION RATING

LASER creator Pat Blount has been in the note business since the late ’80s. He’s flown around the country to more than 2,000 banks and has sold many billions in non-performing notes. Pat put together the LASER system in response to a Request for Proposal (RFP) from the FDIC for a note-evaluating system.

LASER is the Loan Acquisition Suitability and Evaluation Rating system. There’s a reason it’s called that and not the “Loan Valuation System.”

HOW DOES LASER HELP?

LASER asks you 25 or 30 questions about the note. You take the numbers of your ratings, and then use that figure to decide if the acquisition is appropriate based on your desired returns and investment criteria.

You start with a strategy. Then you ask a series of questions to evaluate whether the note purchase will help you achieve your investment objectives.

This system is not the same as the note valuation process; the buyer and seller must establish value together.

When you buy notes, you should evaluate three main components: the loan, collateral, and seller criteria. Your strategy and the types of notes you’re buying will dictate the importance of each and the questions you ask.

{kind=link}

{kind=link}

{kind=link}

Step 4: Making an Offer to Buy Notes

Due diligence should also be part of the “Making an Offer” phase. Sometimes you’ll get a tape first, evaluate it, and then make an offer on it. Sometimes you’ll have to make an offer and then do your due diligence; often it’s both.

You should always have an attorney involved in your note purchase. We’re the property and note-buying experts, not attorneys. We’re not qualified to offer you legal advice, but we can definitely shed light on how to buy notes from banks.

IF YOU’RE BUYING DIRECT FROM A BANK

The bank will usually hire an attorney for the note sales process. If you’re involved in a transaction without a bank attorney, it’s probably because you’re buying the note(s) with a non-negotiable contract written and approved by the bank’s attorney.

The workout, or special assets, or secondary marketing manager that you’re working with represents an organization worth between ten million and hundreds of millions (maybe billions) of dollars. These organizational reps aren’t shooting from the hip on legally binding contracts.

NEGOTIATING BANK NOTE PURCHASES

Negotiating with banks to buy non-performing paper and brick-and-mortar assets doesn’t have to be daunting. Most bankers and mortgage lenders trade these assets every day.

The mechanics of these transactions are relatively straightforward. Though dealing with any large financial institution can have its challenges.

Normally these obstacles center around fragmented processes, inefficiency, and slow timelines. It’s a little like dealing with a government agency. But the rewards can be great.

KEYS TO BANK NOTE BUYING SUCCESS

- Deal directly with key decision makers

- Build relationships with bank reps in charge of approving deals

- Make the bank confident in your ability to perform and close on time

- Demonstrate the benefits of your offer to both the institution and person that needs to sign off on it

How Much to Offer for Notes

Current note values and personal preferences help determine the right amount to offer for notes. Off-market notes can present great discounts and valuable investing opportunities thanks to less competition.

WHAT DETERMINES A NOTE’S VALUE:

- Down payment

- Seasoning

- Credit score

- Number of payments left

- Interest rate

- How interest is calculated

- Note lender type (private owner financed or institutionally originated)

- Amount of installment payments

- Future value

- Loan type (balloon or fully amortizing)

- Debt-to-income ratios

- Maturity date

- Status of performance

- Value of the underlying real estate collateral

- Local real estate market conditions

- Alternative investment options

How to Make an Offer to Buy Notes

OFFER PROCESS

How the offer is made will depend on the seller’s process and could involve various methods.

Bidding: Open or Sealed Bids

Banks that regularly sell notes to individual investors might employ structured bidding processes. In this case, the forms, timeline, contingencies, and deposits are thoroughly spelled out and non-negotiable. This process puts bidders on a level playing field, and the bank can maintain a firm expectation of terms and closing timelines.

Letter Of Intent

A Letter Of Intent (LOI) gets negotiations started by outlining the terms, timelines, and contingencies for your purchase. LOIs may include binders (monetary deposits showing intent).

Indicative Bid

An indicative bid is an offer to purchase with contingencies tied to due diligence factors. Once you place an indicative bid, you’ll gain access to the note’s documents and bank details. Most banks require bidders to sign a non-disclosure agreement (NDA) before releasing note records.

Offer to Purchase Leading to Purchase and Sale

In this process variation, you’d first submit an offer (or LOI or Indicative Bid), which likely includes a binder and outlines a due diligence period. The offer also contains details about the more thorough Purchase and Sale agreement that you’ll complete before closing.

BINDER

A binder is the money you put down upfront to prove that you’re serious. Binders are typically only at risk if you violate one of the Purchase and Sale agreement terms. Required binder amounts vary, but 10% of the purchase price is common.

A binder isn’t always required. Sometimes you’ll get a free look for a short period and then be expected to go immediately to close without any offer or binder.

DUE DILIGENCE

The due diligence period for buying notes is typically short. I’ve seen note deals close in as little as five days with minimal paperwork, and I’ve seen large commercial note deals drag out much longer than anyone wanted (usually due to suspect paperwork, title issues, etc.), but you can expect somewhere between seven and 30 days max. If you’re not able to perform in that kind of time frame, this might not be the business for you.

ESCROW

Binders and deposits should be held in escrow if you anticipate delays in your process and contract. Reputable sellers will not ask you to blindly give them cash or a wire. A reputable seller understands that all of the parties in the transaction need to get what they came for and be comfortable with the process.

Typically the seller’s attorney or agent will hold escrow. There are times that you will make an offer to purchase notes and then immediately close with no escrow or binder.

Step 5: Closing Your Note

You’ve found notes to buy, evaluated them, and decided to make an offer. Your offer has been accepted, and it’s time to close and take possession of the note.

To close on your note, you’ll need to deliver the rest of the funds. This typically happens by wire.

You also need physical possession of the following documents, including (but not limited to):

- Copy of the mortgage or deed of trust, reflecting the same records on file with the county or municipality.

- The promissory note originally signed by the borrower: This document is the note that you’re buying! The “note” lays out all the terms of the debt and each party’s rights.

- The assignment: This document establishes you as the lender. Assignments should have borrower and seller signatures and are sometimes outlined in the note itself or as a standalone document. If the document is attached, it’s referred to as an allonge.

- The file: The file contains all note-related documents and communications. Bringing the file isn’t a requirement, and frankly, you probably won’t get it, but it is nice to have on hand during commercial note transactions. Don’t count on getting it. Do ask for it.

That’s it, now you’ve purchased a mortgage note!

After you close on the note, you’ll need to begin servicing.

WHAT IS NOTE SERVICING?

Note servicing is the process of handling and tracking payments a borrower makes on a note or loan, so note investors don’t have to manage it. If you buy a performing note (the borrower is making regular payments), or you can work with the borrower to get a non-performing note to a re-performing status, consider hiring a note servicing company to collect and disperse funds each month.

Note Investing Success

Mortgage note investing is an excellent way to boost your portfolio. With a little research and top-notch insight from the Distressed Pro team, you’ll have the resources and confidence to buy your first note. Check back with us for guide updates, or dive into the details with one of our free training webinars. You can also subscribe to our BankProspector software directly here.

When it’s time to find out how to sell your mortgage note instead, we can help. Our mortgage note-selling guide covers five ways to sell mortgage notes.

Whether you’re buying or selling, mortgage notes offer flexibility, security, and creative ways to profit. Have any note investing tips or success stories? Comment below – we’d love to hear them!