Non-Performing Mortgage Notes for Sale [8 Sources]

In this article, I review 8 different sources for non-performing notes for sale. You’ll get links and overviews for each type of seller of non-performing notes so you can determine which are appropriate for your business.

Where you start looking for non-performing notes for sale comes down to these 3 questions:

- What types of non-performing notes are you buying?

- What volume of non-performing notes are you buying?

- Do you intend to broker, flip or wholesale non-performing notes as part of your business?

Let’s start with the last point first.

A lot of people ask me how to get started in the note business with no money. There are two answers. You either:

- Raise money from other people and become the managing partner.

- You broker, flip, or wholesale the notes to investors who do have money.

When you’re brokering, flipping or wholesaling you absolutely must be finding your own notes. If this isn’t you then you can skip down to here.

Where to Find Non-Performing Notes for Sale that You Can Broker, Flip, or Wholesale

Finding the deals is the most valuable, highest paid activity in the business.

NOTHING happens until someone finds a deal. Right? Most people don’t have the gumption, the stones, to do what it takes to find deals which is a shame but is also why it is so highly paid.

Finding deals is the highest-paid lowest risk activity in the note business.

Finding the deals in the note business takes the least amount of risk, the least amount of money, and offers the highest ROI in the business. Yes, the money is transactional and not residual like owning notes but if you have more will and time than you have money this is where you start.

Remember that….

(s)He who controls the seller controls the deal.

What that means is that you cannot flip, broker, or wholesale non-performing notes successfully if you’re in a broker chain – because you do not control the seller. At least not successfully and not without trashing your reputation.

You might be able to find one single note and then convince some sucker unsuspecting victim person to pay you a margin on top of what the note cost you even though you paid a retail price, maybe – but that’s not a business model, its not honest and it’s not something you can pull off very many times.

Your buyer will probably end up losing money and your reputation will suffer. This is a small community and the Internet makes it even smaller. Nothing gets people talking like losing money, just try it and see…

Don’t Get Into Broker Chains and Pretend You’re Direct

Don’t embarrass yourself by just becoming an extra middleman – this is what’s not so lovingly referred to in the business as a “joker-broker”. Its a sad place to be, you look silly, and any investor who is worth working with will discover the charade with a few easy questions.

You Must Be Direct to the Seller to Flip, Broker, or Wholesale Notes

You must have your own source of non-performing note deals, not other middlemen, if you are going to flip notes, broker them or wholesale them. Period.

So enough of me being a downer, let’s stop talking about where you can’t buy notes and start talking about where you can buy notes.

Non-Performing Notes for Sale- 8 Sources

I’ll review each one, provide you some links, and recommend each based on the asset type, volume, and business model decision points mentioned above so you can determine which of these note sellers is right for your business.

- Big Banks

- Local and Regional Banks

- Credit unions

- Special Servicers

- Hedge or Private Equity Funds

- Brokers

- The FDIC

- Marketplaces and Listing Services

I should note before we get into this that we have services and training for you if you determine that you should be buying notes from banks, credit unions, or servicers or if you want people to send you deals as an investor.

1. Buying Non-Performers from the Big Banks

Let’s define “big banks” first – big banks are the top 10-15 banks. I’d say top 20 but since one of my best clients was a top 20 bank I’d hate to steer you away from that same opportunity.

The big banks are constantly selling non-performing notes (and REO). The problem for most investors is the size of the pools that they’re selling and the requirements for getting “in” and getting approved as a buyer. A few things to know about the buying NPNs from the big banks.

- It is extremely unlikely that they will sell you a single non-performing residential note. There are some gurus out there who will tell you to find a distressed home owner have them introduce you to their bank and then you buy the note from Bank of America – I’ve NEVER heard of this working. I’ve never heard even one first-hand account of this working at a big bank.

- Some of the largish banks do have trading desks where regular investors can buy notes. You simply have to speak with the right person and get approved.

- I have seen success with buying one-off non-performing commercial notes from big banks. Wells Fargo, for example, has sold non-performing notes each of the last 6 quarters and they seem to have a some reasonably autonomous commercial workout officers in regional workout centers who are empowered to make decision on small balance commercial notes.

It’s worth mentioning that banks don’t hang a sign out that says “non-performing notes for sale” – but that doesn’t mean they aren’t. In the next section we’ll address that a bit.

Bottom line:

- Type: Big banks sell all types of non-performing notes

- Volume: Big banks typically only sell very large volumes of notes with small balance commercial as the rare exception.

- Bottom Line: Any loan sale advisory for the very big banks will most likely be done with a big name broker. Most successful direct buyers will be large funds. Not suitable for the unproven broker or investor.

2. Regional and Community Banks

For many, regional and community banks can be the sweet spot for where to buy non-performing notes. As an auctioneer and broker these banks were my “bread and butter” for note, REO, and foreclosure sales.

There are more than 6,000 banks in the U.S. and only the top 10 to 15 are, well, the top 10 to 15… the rest fall into this category. You can find non-performing notes for sale with many hundreds of the thousands of banks in the U.S. You just have to know where to look.

The thing about working with the smaller banks is this:

- They’re not so big that a small sale won’t impact their books

- You can easily speak with a real person who can make decisions (unlike the big banks)

- They tend to do their own loan workouts instead of farming it out to a special servicer

- These banks are repeat, non-emotional sellers of non-performing notes and REO

- A few small banks can make you a full-time book of business

The challenge with calling on the smaller banks is that there are SO MANY. Where do you begin?

- Which banks are sellers and which aren’t?

- What do they have on their books?

- Who do you talk to about selling?

- What do you say?

At least these were my questions when I first started out back in late 2006. Maybe you’re asking some of these questions now…

It was having found the answers to these questions that originally drove me to create this site in 2009.

What I learned was that each quarter banks report a lot of information about their late and non-performing notes as well as a whole slew of “health” and “sell” indicators (as we call them). Its with this information that you determine which of the thousands of lenders you should be pursuing.

You can get this info from the FDIC like I show you in this video.

But if you’re serious about finding non-performing notes for sale from lenders we make it MUCH simpler with BankProspector.

Bottom line:

- Type: Community and regionals banks sell all types of non-performing notes

- Volume: Regional and community banks can sell everything from individual notes to pools.

- Bottom Line: Brokers and investors should shoot to work with 5-10 regional and community banks.

3. Buying Non-Performing Notes from Credit Unions

There are nearly 7,000 credit unions many of them have non-performing assets that they’ll sell. Credit Unions report separately from banks but their reporting is still public and it gives us clues as to which credit unions will have non-performing notes for sale.

We track the non-performing loans and foreclosed and repossessed assets for every credit union in the US. Working with credit unions is very similar to working with banks with a few differences.

- Credit unions can be extra sensitive to their reputation, they serve members (often) of a small(ish) community

- Most credit unions are really small so they don’t have a ton of assets but the ones they do have matter to them

- You can get right to top officers because they’re so small.

- Credit unions are regulated by the NCUA rather than the FDIC that means that you’ll research them differently.

Bottom line:

- Type: Credit unions can sell all types of non-performing notes, a lot of what they have is residential but there are plenty of credit unions making business loans as well

- Volume: They can sell everything from individual notes to pools.

- Bottom Line: Anyone in the note business, regardless of business model, should be working with 5-10 credit unions.

4. Buying Notes from Special Servicers

A servicer handles the administration of a loan or pool of loans on behalf of or in partnership with the owner of the loans. Servicers will frequently deal with offering non-performing notes for sale.

A special servicer handles the administration, collection, workout, and sometimes disposition of problem loans as well as the sale of REO. We maintain a growing list of loan servicers, special servicers, BPO and REO asset Management companies here.

Some special servicers will have a defined way that they sell “retail” individual assets, some sell pools, some do both. You’ve probably heard of some of the big ones like BayView and OCWEN.

- Type: Some servicers will specialize in one type of property or loan so you need to make sure you understand what they’ve got.

- Volume: A few servicers sell “retail” one-offs others sell pools, many because they mostly service the big banks will foreclose and sell the REO.

- Bottom Line: Investors should look into which servicers might be appropriate for your business model. If your’e acting strictly as a note broker then this probably isn’t a great seller for you.

5. Buying Notes from Hedge Funds and Private Equity Funds

Hedge (and private equity) funds buy large pools of non-performing notes for sale from the largest banks and other high volume sellers. There are a few “exits” that hedge funds use.

- Foreclosure and then sell the asset REO or else put a tenant in it and rent it.

- Workouts (loan modifications) where the goal is to get the borrower paying reliably.

- Wholesaling where a fund buys a large pool, retains some portion of it, then sells the rest to smaller investors.

Hedge funds can buy much larger pools than most individual investors and firms that specialize in this are set up for it.

Frequently a fund will slice up the pool and find different ways to make a return on different sets of loans. They’ll obviously keep the most profitable. Smaller funds or even individuals then buy the remainder.

Its not uncommon for a hedge fund to have a specific time frame that they want to be in and then out of an investment. After a fund or investment has run its course and made its returns the fund manager might look to clear the rest of the assets off it’s books and move on.

Hedge funds don’t have to do the same type of public reporting as banks and credit unions so if you want to pursue this avenue you need to do a little homework. You can buy lists of hedge funds like this one but you can expect to pay at least a few thousand dollars for it.

- Type: Funds tend to be very specialized but you can find funds that specialize in either commercial or residential.

- Volume: Larger funds sell larger volumes, and smaller funds have been known to sell even individual assets.

- Bottom Line: Hedge funds can be a good source for small and individual investors and bigger funds feed the smaller ones. A lot of chicanery happens around the smaller funds when it comes to brokers sadly. Much like the joker-broker, I warned you about at the top of this post if you’re in the business for a little while you’ll find someone trying to sell you notes that belong to one of the funds. Don’t do this. If you’re going to buy a pool or get things re-performing then re-sell your notes that work. If you’re going to pay retail for one-off notes then try to flip those to an unsuspecting noob that business model is no good for anyone.

6. Note Brokers and Loan Sale Advisors

There are a few big non performing debt sellers like DebtX and First Financial as well as other note brokers and intermediaries (many of whom are BankProspector subscribers) and increasingly a long list of smaller independent players in the market who offer non-performing notes for sale.

The thing you have to watch out for with note brokers is – well – you need to make sure they’re for real.

What tends to happen in this business is that a broker will get a hold of a tape and send it out, then another “broker” gets a hold of the tape and passes it on and this continues, sometimes indefinitely. I know investors who have had their own tapes shopped back to them because the “broker” was so removed from the actual source and so removed from the real seller.

“Brokers” who haven’t managed to get a business email address… Who say they have a buyer who needs to buy X-100s of millions of dollars of product a month (but they’re telling you on LinkedIn…).. brokers who can’t tell you any details about the seller or can’t answer questions for you about the assets on the tape – these folks aren’t for real and should be avoided.

Work with reputable brokers and loan sale advisors not LinkedIn and newsgroup hucksters.

- Type: All types of loans.

- Volume: Completely depends on the broker. Everything from one-offs to large pools.

- Bottom Line: Can a broker broker notes another broker is brokering :-? …. Mostly no. Brokers and loan sale advisors are great for investors not other brokers.

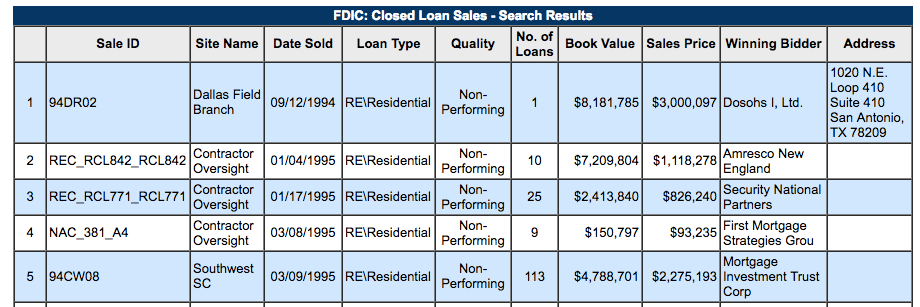

7. FDIC Loan Sales

The FDIC frequently has non-performing notes for sale. You can find info on their past loan sales here. The FDIC sells its loans through 3 loan sale advisors.

- DebtX

- Mission Capital

- First Financial

You do have to get approved as a buyer. You can learn more about the process here.

- Type: All types of loans (and other assets).

- Volume: Check out the past sales list excerpt below, everything from 1 to 100s of notes.

- Bottom Line: These sales are for investors, there’s no broker participation offered outside of the 3 approved loan sale advisors. If you can get on the list of approved buyers DO IT.

8. Loan Sales Marketplaces

In recent years various marketplaces have been coming and going. These can be decent sources but the truth is that they’re probably better for the seller than the buyer. Whenever you bring a deal to a big enough mass of bidders the sale should find a true market price. This is in stark contrast to the more “off-market deals” like what you’ll find when you go direct to lenders and services.

One marketplace that is showing a lot of promise is the Paperstac. They always have non-performing notes for sale, they provide extensive information, and you can tell it’s built by a real “note guy” (I’ve interviewed him, he’s real) because all the steps and processes that you would want or need for the transaction are built right in.

Non-Performing Notes for Sale – Summary

If brokering notes is going to be a substantial part of your business then the marketplaces and other brokers aren’t going to be good sources for you. You’re going to need to find your own sellers and in order to do that, ideally, you’ll prospect loan originators like banks and credit unions, and yes, private mortgage note holders.

If you’re looking to invest with your own money or as a fund then you have more options and where you should find your notes for sale will be largely driven by the volume that you need.

If you’re an individual investor and you’re looking to user your SDIRA to get into a small handful of notes then calling on lenders and originators probably isn’t going to be the best use of your time. On the other hand, if you’ve got significant funds to deploy then some of the bigger note sellers are going to be good for you and it would probably also make sense to have a prospecting plan in place in addition to working with larger hedge and private equity funds, the big note brokers etc.

If you’re just starting out and you’re going to do some brokering, flipping, wholesaling then you it really is necessary that you find your own sources for deals and that’s going to mean rolling up your sleeves and contacting some lenders.

Continue Reading