Insider’s Guide to Buying 2nd Mortgage Notes

Would you like to learn how the most successful mortgage investors are buying non-performing mortgages for Pennies on the Dollar? You are about to learn the insider secrets to buying discounted second mortgage notes.

Investing in second mortgages or “junior liens” isn’t a very well-known sector of note investing but can be the most profitable if you buy them direct from the source.

In this post you will discover what makes 2nd mortgages so lucrative and the cheapest places to consistently buy non-performing second mortgages.

You will learn:

If you’ve been looking into investing in notes then no doubt you’ve come across second mortgages as one investment that a lot of people are excited about in this industry. If you’ve been wondering how seconds work, why people invest in them and what makes them profitable, especially when they’re non-performing, then you’ve come to the right place.

What is a non-performing 2nd mortgage

When we talk about a second mortgage we’re talking about a promissory note loan that is in a junior position to a senior note. When we talk about debt being senior or junior this has to do with the priority of the note with regards to pay off especially in the case of default.

There are two types of seconds, your traditional second mortgage, which is amortized over a traditional schedule and is used by some home buyers when they don’t have enough of a down payment.

The other type of loan that’s a second is a HELOC or home equity line of credit, which is a type of debt that is closer to credit card debt than it is a mortgage but nonetheless is secured by the house in a junior position to the first mortgage.

So when we talk about seconds we’re talking about any mortgages or loans that are secured by the property that in terms of lien priority come after the first mortgage.

A non-performing note is a note that hasn’t been paid for 90 days or more. So a non-performing second mortgage is any of these junior liens, HELOCS or seconds which are 90 days or more past due

Click here to Download the Non Performing 2nd Mortgages PDFWhy invest in non-performing second mortgages

At first blush it may seem crazy to buy a loan that isn’t being paid and that has other loans that are superior to it. But stay with me, I’m going to try to demonstrate to you why a lot of investors find seconds so attractive.

There are a variety of ways that second mortgage note investors get paid off and make profit. In some cases you’ll modify the loan, you may reduce the principal for your borrower, extend the term, reduce the interest rate, or offer other kinds of relief that allow the borrower to continue to pay and allow you profit.

The second lien holder will also be paid if the property is refinanced or sold. Your loan will have to be taken out, that is to say paid off,before anything can be done with the property. Depending on the market that you’re, in even if the house is foreclosed on by the senior lien holder, you still have a good opportunity to get a return on your investment in places where home values have soared.

Investing in second mortgage notes allows a lot of experience with a variety of cost and more importantly provides huge upside potential because of the dirt cheap pricing of seconds.

You can buy non-performing second mortgages for pennies on the dollar

Non-performing second mortgages can sell for pennies on the dollar. Quite literally. And that’s how the pricing of non-performing seconds is referred to. For example you might pay $0.06 or $0.12 which means would mean 6 or 12% of the unpaid principal balance on the note.

One of the keys to doing well with non-performing second mortgage note investing is to spread your risk across a number of loans. Typically a second mortgage investor won’t buy just one loan, they buy number of loans knowing that they will not get paid on some of them because the first position will foreclose and there won’t be enough equity but the ones that they do get paid on have such high margins that it more than makes up for the losses.

Click here to Download the Non Performing 2nd Mortgages PDFWhy are 2nd mortgages sold so cheap?

Non-performing second mortgages are cheap because they’re often not worthwhile for lenders that service them to work through. We’re generally talking about small balance low and mid 5 figure debts.

In many cases the lenders don’t have the same kind of flexibility in their workouts that a private investor would have because institutional investors, like banks and credit unions, are heavily regulated, while private investors have much fewer regulations with which to contend.

So second mortgage notes are being sold on the cheap because it’s not worth while for the institutional lenders to throw a lot of manpower and resources at collecting the small balance, possibly questionable, debts.

Why Banks Want to Liquidate Non-Performing Second Mortgages

The reason banks want to dump non-performing “second mortgages” or junior liens is because they have a disproportionate negative affect on their balance sheet.

Bear with me here, The reason I dwell on what’s going on underneath it all and on the data is because it’s that knowledge that is going to help make you a professional. If you don’t know why you’re doing what you’re doing then very often you’re not going to do it very well (I want you to do it well ) and beyond that you’re going to miss opportunities.

You could be having a conversation with a workout officer and zzzzoom, stuff she’s saying goes right over your head. You’re wondering what she was talking about, she gets the sense that you DON’T know what you’re talking about or in any case there’s that silent chill that happens when two people fail to connect and then poof… no relatability and you are o-u-t out. So… Consider this guidance from the FDIC website:

Under the proposed rule, 1-4 family residential mortgages would be separated into two risk categories (“category 1 residential mortgage exposures” and “category 2 residential mortgage exposures”) based on certain product and underwriting characteristics. The proposed definition of category 1 residential mortgage exposures would generally include traditional, first-lien, prudently underwritten mortgage loans. The proposed definition of category 2 residential mortgage exposures would generally include junior-liens and non-traditional mortgage products.

WHOAAA, if you read that and it just makes you dizzy and you hate it let’s back up and break it down. Here it is – there are 2 categories of risk for residential liens. Second mortgages (second position mortgages) fall into the second. Now consider this table below. Second mortgages are in the second column. Look it over. I’ll meet you at the bottom of the table.

| LTV ratio | Risk weight Cat 1 residential mortgage | Risk weight Cat 2 residential mortgage |

|---|---|---|

| Less than or equal to 60% | 35% | 100% |

| Greater than 60% and less than or equal to 80% | 50% | 100% |

| Greater than 80% and less than or equal to 90% | 75% | 150% |

| Greater than 90% | 100% | 200% |

So this begs (at least) 2 questions.

- What’s risk weighting?

- Why does this make the non-performing second mortgages worse for banks – what’s the impact?

Risk weighting is just what it sounds like. Some loans are riskier than others and so different “weights” are assigned and those weights then impact the balance sheet and in this case we’re talking about capital adequacy ratios. Banks have to maintain certain levels of capital and you can read more about that here or here.

In short, the calculation puts capital as the numerator and risk weighted assets as the denominator. Therefore the bigger the denominator (the risk weighted assets), the lower the ratio, – the bigger the drag on CAR (capital adequacy ratio – remember division? denominator down, numerator… nup).

If CAR falls below acceptable levels then red flags are raised, regulators move into the cube next to you and there’s a real risk that you’ll be shutdown if the problem persists (if you’re a bank).

As you can see in the table above, in the far right column (category 2), second mortgages are weighted much higher than first position liens (category 1). At the top end of the scale junior liens are weighted at 200%.

Thus, disposing of troubled second mortgages (junior liens), pound for pound, has disproportionately more positive impact on a bank’s balance sheet.

Banks can cash those juniors out by selling them to you. They recover what capital they can and their ratios improve.

Second mortgage note investing strategies.

The first step to making money with non-performing 2nd mortgage notes is to find them.

Where you’ll be able to source them from depends on how much capital you have to work with and how much work you’re willing to do.

If you have ready capital and you don’t mind paying a premium for then our first investment strategy might be the right one for you.

1. Buy from brokers.

The easiest way to buy non-performing junior notes

Some large private funds, frequently ‘hedge’ funds, will buy pools of non-performing juniors seeking opportunistic returns. They might workout or foreclose on some loans in this pool, carve it up and sell off other pieces to smaller investors. Often then that investor will carve up the pool further and might even sell notes directly to the final buyer.

The challenge with taking this approach to acquiring ‘seconds’ as they’re often referred is 3-fold:

- If you’re the end buyer you’re getting very picked over assets, the bottom of the barrel

- Each “middle man” or step between the original source of the loan and the end buyer makes a margin on his sale which means if you’re at the end of the line you’re likely paying too much.

- The nature of notes, especially seconds, is that the paperwork must be in order if you’re to have any ability to exercise your rights as the lender (foreclosure, collection, etc)

How to Find and Buy Non-Performing Notes from [A-Z]:In this article we cover how to find non-performing notes, how to buy them, you’ll learn some strategies that others take with non-performers and there’s some downloadable bonus material.

2. Buy direct from banks

The most profitable way to make money with non-performing junior liens requires more work

As you know banks and credit unions make loans…Sometimes these loans are originated for the express purpose of then selling them on the secondary market, sometimes the loans are originated to be held on the bank’s books as “portfolio” loans.

That is to say “whole loans” (non-securitized) originated and held for the purpose of collecting the payments form the borrower.

Many banks will sell non-performing second mortgages rather than trying to work them out or resolve them internally. Your job then is to find out which banks are selling the types of assets you want to buy, find a decision maker, and then be there when the lender is ready to sell.

How to Buy Notes from Banks [Complete Guide] We created a step-by-step “How-To” guide on buying notes from banks and specifically buying non-performing mortgage notes and real estate notes, direct from banks.

Click here to Download the Non Performing 2nd Mortgages PDFMake money buying non-performing second mortgages

They say in real estate that you make your money when you BUY the property. The same holds true when you’re buying notes. If you’ve overpaid there’s virtually no way to recover your investment.

One way to make a return on your investment is to ‘workout’ the note, that is to say, you get the borrower to start paying again.

When a borrower stops paying on their second mortgage default interest and arrears accrue. Most of the time, part of your workout strategy will include getting the borrower to catch up on the arrears and default interest.

When there’s equity in a property an investor can get a return on his investment by foreclosing on the property. Yes, junior liens mortgages in any position usually have the power to collect monies owed through the foreclosure process. Of course if there’s no equity to cover the second position then foreclosing does not help you get a return because foreclosing lien holders always have to pay superior liens.

What that means is that if you own the HELOC on a property that also has a first position mortgage, a second position mortgage, and back taxes, all of those will have to be paid from the proceeds of the sale BEFORE you will see any money in last position.

Trying to make a business out of trading junior liens is doable but you’re going to have to learn a few thing:

- How and where to source notes

- How to evaluate a “tape” (the spreadsheet of loan information you’ll receive)

- How to negotiate a pricing on a tape

- How to submit your offer to purchase, LOI, or “indicative bid”

- How to evaluate the collateral (paperwork, loan documents)

- How to close on the sale and take possession

- How to workout the loan

- How to service the debt

- How to transfer your rights in a sale

It looks like a lot. And it is.

But the money in trading notes can be HUGE once you figure out what you’re doing.

Arguably, the first step in the note business is to be able to source the assets. Nothing happens until you have “product” to evaluate and bid on.

If you’ve got experience working with banks and you need portfolio information and contacts to grow your business then have a look at BankProspector. If you’re just getting started and have never worked with a bank before then have a look at the Academy. If you’re an investor with more cash than time, then have a look at the Verified Investors Program.

Frequently Asked Question

Which banks have non-performing junior residential liens?

The list of course changes from time to time but this list of banks has junior liens in “nonaccrual”the most troublesome loans on a bank’s books and this is a list of banks with 90+ day late junior liens(also considered non-performing). HELOCs “home equity lines of credit” are also “junior liens” and you can find a list of banks with those 90 days late here and a list of banks with HELOCs in nonaccrual here

What kind of discounts can you get on non-performing second mortgages?

This depends on the collateral, who’s selling, the borrower’s status and a host of other factors but you could pay anything from literally a penny on the dollar up to 30+ cents.

How many banks have non-performing junior liens?

Thousands of banks have portfolios with non-performing junior liens

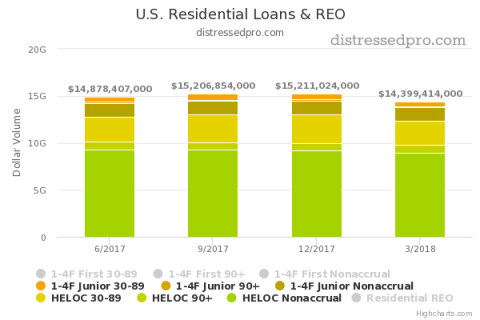

What’s the dollar volume of non performing 2nd mortgages today?

At the time of this writing a little more than $17Billion

How do I get bank’s to sell their 2nd mortgages to me?

If you’re looking to learn how to work with banks and their distressed assets you should checkout The Academy

Got a question about non-performing second mortgages? Ask me in the comments box below.

Click here to Download the Non Performing 2nd Mortgages PDF