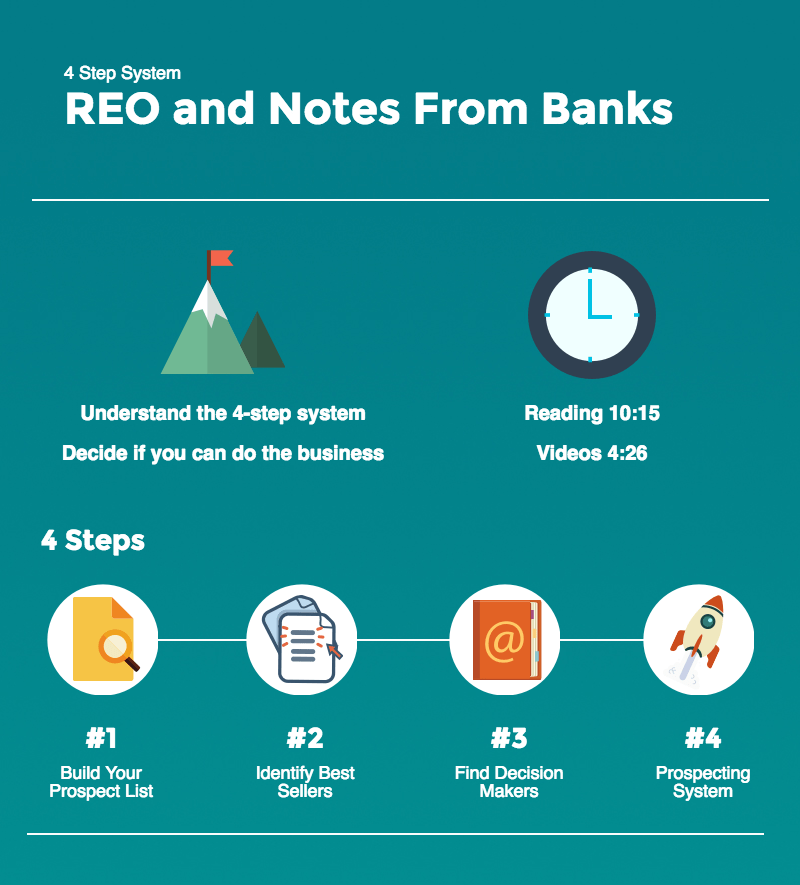

4-Step System for Buying Distressed Assets Direct from Banks

Banks are the best and most reliable source of REO and mortgage note deals. If you want to buy the cheapest REO properties, going bank direct will get you the best prices.

In this post, you will learn how to implement our proven 4-step system for sourcing bank direct distressed property and note deals.

Finding the deals is the most valuable role in the business and that’s what you’ll learn in this post. Our 4-step system will show you how to create a steady stream of deals from your target banks, like many of our students have done.

You will learn:

Why Lenders Should Become a Primary Source of Deals for You

Lenders, banks, and credit unions are repeat sellers of distressed and discounted assets. Let’s say that one more time.

Banks are repeat sellers of discounted and distressed assets.

There isn’t another opportunity in real estate where you can say the same thing.

Who but banks sell distressed assets more than once – to the same buyer no less!? The most savvy of you will say “bankruptcy trustees” and you’d be right but short of that small club the answer is lenders – banks and credit unions.

Banks sell non-performing notes and REO as a regular part of their day-to-day business. If you’re willing to take the time to learn how to tap into this source of deals you can change your business, and possibly your life, forever.

What if you could do just 5-10 deals per year with just 5-10 sellers…?

Why that’s 25 – 100 deals per year! From just 5-10 sellers!

How much would your life change if you were no longer forced to suffer on the hamster wheel of private seller prospecting? It’s exhausting. It’s inefficient. And you are not in control of your deals or even your days.

What if, instead, you got calls and emails from a handful of institutional sellers who know that you’re the person to reach out to when they have REO or non-performing notes they need to sell?

It’s a game changer.

The biggest problem is that most people start out going after all the wrong banks. They call on Wells Fargo, or Chase, or Bank of America. Then they say “it doesn’t work,” “the banks don’t sell,” “it’s a waste of time.”

Why engage in the brain damage that is working with a huge bank when there are thousands of other lenders in the U.S. who are vastly easier to work with? It makes no sense and it’s frustrating and fruitless.

So without further ado, let’s dive into the 4-step system.

Step 1: Get a List of REO and Note Seller Prospects

Here’s a fact about any prospecting or marketing…

Your prospecting and marketing efforts are only as good as your list.

Even if you’re a silver-tongued sales dynamo who can sell you-know-what to a dog, your skills are worthless if you are going after the wrong prospects.

Targeting the right prospects is the first critical step in succeeding with finding REO or note deals.

You have limited resources. We all have limited resources.

We only have so much time in a day, attention span, marketing budget, and wherewithal. Therefore you must be vigilant in making sure that you’re using your resources wisely. Picking up a directory or a guide and dialing for dollars is over. Brute force, blind cold-calling is an insult both to your intelligence and to your prospect. Calling on anyone and everyone is a waste of your time. Don’t do it.

If you’re doing the thankless work of calling on hundreds of private property owners then you have the luxury of messing up a bunch along the way … “NEXT!”

If you’re targeting 50 or 100 big repeat note and REO sellers like banks or credit unions where the right relationship could make your year or even your decade…How many of those do you want to mess up?

Here’s a proposal. Do your homework before you ever begin and start your prospecting with a really excellent list.

How to get a prospect list of banks and credit unions for notes and REO:

They report things like…

- How much of each type of bank owned property (REO) they have on their books

- How much and what kind of non-performing loans they have have for each asset type

- Whether or not they’ve sold any non-performing loans

And a whole bunch more.

With all this information out there, it makes no sense for you to prospect blindly.

3 Good Reasons You Should Do Your Research Up Front

- Your preparation will be recognized and met with respect. You’ll be perceived as professional.

- You’ll have more confidence about what you’re saying and who you’re saying it to.

- You will do more deals.

Would you rather call 10 targeted prospects who have exactly what you need 10 times each or call 100 prospects and be totally clueless? The answer is obvious.

But I digress… we were talking about getting a prospect list together.

2 Free Websites You Should Use to Get Your First Lender Prospect List

1) FDIC.gov – the Federal Deposit Insurance Corporation

The FDIC’s website is excellent for getting together your first rough list of prospects. It is not excellent at giving clear easy-to-read stats on individual banks, and you’ll likely want to research how info is organized within the site. Data is on the raw side, so you’ll need to know exactly what you’re looking for and what to do with it. Side note: the FDIC website is only for banks, not credit unions.

2) NCUA.gov – The National Credit Union Administration’s Website

The NCUA website is where you can unearth credit union data and is the best and only place to get a list of credit unions (other than BankProspector) with non-performing loans and foreclosed and repossessed real estate. Side note: the NCUA website was clearly built by the government and is about as user-friendly as a rusty bear trap.

Action Step #1: Get Your First List of 100-200 Lender Prospects

Once you have this list together, hopefully this will all start to seem real, and you’ll have a tangible, conquerable workload that you can put into a prospecting system – and this will be the beginning of your path to success.

Register for a Fee Web Class and Demo Now

Step 2: Qualify Your Prospects BEFORE You Begin Prospecting

If Step 1 is starting with the right list then step 2 is scrubbing that list.

It’s one thing to go and download a list of 100 or 200 banks with REO or non-performing notes, it’s another to really have insight into what’s going on with their portfolios and their motivations.

This may sound like a bit much but stick with us.

7 Key Qualifying Questions You Can Answer Before You Even Speak with a Banker

If time is our most precious resource and we want to invest it as wisely as possible then doesn’t it make sense that we focus first on our most valuable and likely prospects?

If you answer “yes” to that question then the natural follow up is “How do we know which prospects are our best and most valuable?”

To answer that question we can look to the numbers. If you don’t have BankProspector, then the next best way is to use the FFIEC website.

Use the FFIEC Website to Download Individual Bank Reports to Answer 7 Key Questions

Before you invest more time, find the answers to these questions:

- Is the bank healthy enough to sell?

Lenders continue to fail month after month. While many newbies believe that they should be pursuing failing banks, as you’ll learn on this web class, that is a time consuming mistake to make. - What in the portfolio are they prepared or preparing to sell? We can see where they’re making value adjustments. This is an indicator that they’re trying to get real about the value of a portfolio of non-performing assets.

- In which portfolios are they having the most trouble? Some simple math on the total non-performing assets vs the the total portfolio gives you non-performing loans ratios.

- Do they currently have non-performing assets for sale? Banks have special “buckets” or “accounts” where they hold late and non-performing loans for sale.

- Do they have a history of being good sellers? We can see from past history if they are selling their “nonaccrual loans” (late state non-performing loans).

- Are their portfolios improving or deteriorating? We can look to whether or not they are adding or subtracting from their rainy day fund.

- What’s the maximum deal size potential you can expect from this lender? Whenever lenders take a loss by selling to you at a discount that loss has to be taken from a special account. When you’re working with small lenders you can see up front if they can do the deal sizes and discounts you’re looking for.

All these questions can be answered to some degree before you ever even speak with anyone. Amazing, right?

Action Step #2: Scrub Your List and Identify Your Top 50 Best Prospects

Decide on exactly what you’re looking for then educate yourself on how banks sell and what their numbers mean. If you don’t, you are likely to find yourself very frustrated. If you do, it’ll be easier to tackle than it sounds.

You’ll waste a lot less time floundering. You’ll be more competent and confident when you start reaching out to decision makers. You’ll get to do deals much more quickly.

If you’re having trouble figuring this part out consider the next session of the Academy where we cover this in depth.

Step 3: Build a List of Decision Makers at Your Top 50 Priority Lender Targets

Two things are critical in step 3. “Time blocking” or working in “batches,” and aiming high.

Time blocking is absolutely crucial for effective prospecting.

What that means is that now that you have your list of 100-200 banks with a choice list of 50, you need to get together a list of top contacts for each of your top 50.

DON’T go calling them just yet. Hold on. Let’s just get the list.

How NOT to Prospect Well

Bank: “Hello, Some Little Bank, how can I help you?”

You: “Hi, I’m looking for the person in charge of selling your non-performing notes and REO.”

Bank: “What?”

You: “Yes, I’m looking for a special assets manager or someone who’s in charge of selling your notes and REO.”

Bank: “I’m sorry, we don’t do that here”

You: “Oh, really? Is there anyone else I can talk to about that?”

Bank: “Um, sure” [long pause…..] (Hey Bob someone is asking about REO, do you want to talk to them?)

Bob: “No.”

Voicemail: “Hi, you’ve reached the voicemail of Bob Banker…”

And that’s that.

If you’re prospecting this way, you’re going nowhere. This is the “brute force and ignorance” approach. It is so over. This might have worked with persistence in the days of only phones and fax machines. It is not going to work for you today. Maybe it’ll make you feel productive because, hey, you called, right? Nah. Doesn’t count. No reason to even pick up the phone if you don’t have a solid plan in place that will get you to the person you actually need to talk to.

Today? This blind approach is OVER.

If you’re serious and you want to be effective, you need to open by asking for a specific decision-maker by name, and you should start as high up in the organization as you can muster.

How to Prospect Effectively

Call High-Level Decision Makers

Your starting point will vary by the size of the bank. If you’re calling on small community and regional banks in your area you should be calling all the way at the top, like the president.

Really? Yep

There are 2 reasons for this:

- It gives you “posture.” Nobody calling into the bottom of an organization is worth talking to. You can argue this but the fact is that this is the perception. Who calls the operator? Customers and salespeople who have invested no time whatsoever in learning about the prospect they’re calling on, that’s who. So put on your big-boy pants and prepare to get a little bit uncomfortable if you’ve never done this before.

- It shortens your sales cycle and gives you credibility within the organization. Imagine you call the president or senior vice president of an organization, you have a real conversation about their challenges and their portfolio; you’re referred next to the special assets manager who will actually do the work and you say “Hi Bob, I was just talking with Jennifer (your superior) and she said that you and I should speak.” The next thing that happens is you’re invited in for a meeting. Guaranteed.

Get a List of at Least 50 Decision Makers Before You Start Contacting Them

It’s important to get a list of decision makers before you do any calling and emailing or other outreach.

If you save your research for your prospecting time…it will never happen.

Your “research time” will turn into stalling time and procrastination.

Put together your list of 50 BEFORE you start contacting people because in the next step you’re going to begin to put together a prospecting system and this system only works if you have fuel for it. Your list is the fuel.

Resources for Building Your Contact List

There are so many resources available for identifying decision makers, it is inexcusable not to do your homework.

- Bank websites are obvious resources for researching decision maker contacts. Will it be easy to go from bank site to bank site to gather this info? No. Is it absolutely necessary to know the names of the decision makers that you’re trying to reach? Yes. So if you have no other way, bank websites should be a go-to.

- LinkedIn when used properly will help you identify and contact real decision makers.

- There are lots of resources online but don’t forget that there are real people working at these lenders and they belong to professional organizations like TMA, ABI, and local banking organizations. Join these. Go to the events. Get into the community and start building connections.

Action Step #3: Build a List of 50 Decision Makers for Your Top 50 Banks

Go to the bank websites, LinkedIn, wherever you need to and get your list of 50. We cover this extensively in the Academy. Put them in a spreadsheet or CRM so that you can track your activity in Step 4.

Step 4: Build Your Unstoppable Deal Machine

Now you know how to build a list of prospect banks and credit unions with non-performing loans and REO, how to qualify them, how to build your list of contacts.

It’s time to start talking to decision makers. There are a few ways you can do this.

At the end of this post you’ll find a link to a “framework” for prospecting.

Working with institutional sellers is different than working with private sellers. You need to think about what’s in it for them. Are you going to make their lives easier? Help them achieve better outcomes? How do they evaluate what’s a good outcome? In short, what are the internal factors for them that drive the decision to do a deal with you?

Remember, when you get a good repeat seller you’ll do deals again and again, often for years. How much differently would you approach a prospect whose deals could pay off your mortgage in a few years versus a private seller where you might be talking about a few thousand dollars one time?

A “Plug and Play” Prospecting Plan

You should have a fully documented prospecting approach including who to call, what to say, and how you’re going to contact decision makers by phone, email and LinkedIn. Not only that, but you should have a template and a method for each.

You should do this for a few reasons:

- You don’t want to be trying to figure out what you’re supposed to do during the time that you should be doing it. This is a surefire way to get nothing done.

- You have a plan, your prospect doesn’t have a plan to be prospected. This gives you the upper hand. If you have predetermined that if your prospect throws a left hook, you will duck and jab then who has the advantage?

- If you stick to a plan and find that every time you duck and jab you get hit then you know you need to change that play. If every time you make that play you win then you know that you should change nothing and do more of that. If you go with no plan and you simply get punched a lot and hope for the best then you do not know what to change.

Make a schedule and a script for each of the initial interactions. This way you don’t have to think about it; you simply execute then look back and evaluate your results and adjust.

Implement a Simple Tracking System and USE IT

If you’re doing this right then you’re going to have a number of balls in the air at any one time. Don’t try to keep track of these in your head.

You need one single place where you keep track of all of your contacts, the next actions, the conversations you’ve had the follow up that’s required, etc.

The problem most people run into with this is they make it too complicated. If you spend more time wrestling with your software than you do with buyers and sellers, you can’t win. People have been known to succeed in this business with everything from spiral notebooks, to spreadsheets, to full blown CRMs, what you use is up to you.

BankProspector includes a very simple “CRM” – a basic way to keep all your notes , contacts, and next activities for each prospect in one place. You don’t need to use it but you do need to use something.

Action Step #4: Put a Prospecting System Together and Add Your 50 Contacts to It

Here’s the article mentioned above that lays out a precise prospecting plan.

Here’s what you should do now.

- Decide what your prospecting schedule will be.

- Document a plan for how you will first contact lenders (calls, emails, LinkedIn, over what time period, how many contacts, etc.)

- Write a script to use when you call.

- Write a cold email template.

- Write a LinkedIn plan.

- Choose a place to track your activity.

- Add your first 50 prospects to your system.

Become the Go-To Person for All Kinds of Deals

The best way to make money in this business is to become a problem solver who is able to solve problems and therefore make money in a lot of different ways. Here are just a few…

- Refer problem C&I debt to an expert.

- Refer auction opportunities to a national company.

- Learn the different ways to make money with non-performing commercial real estate loans.

- How to flip notes with transactional funding.

- Broker performing notes to other banks.

- Partner in deals where you find them and someone else funds them.

- Use government and other programs to maximize returns.

The list goes on and on. The point is that once you have become the source of the deals the sky is the limit. The more problems and different kinds of problems you’re able to solve the more deals you’re going to get a look at and the more money you’re going to make.

Yes, it absolutely makes sense to start as in one niche but learn to ask the questions to uncover the tertiary opportunities and you will see your income skyrocket.

Hope this article sets you on the path to succeeding with institutional sellers and that it changes your business forever.

Let me know what you think in the comments!