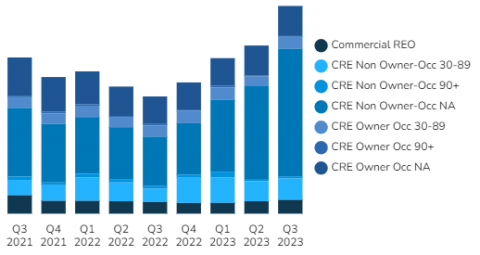

Commercial debt saw non-performing loan volume soar to new two-year highs in Q3.

CRE debt, including construction loans, as well as consumer debt has seen distress escalating in dramatic fashion this year.

Farmland loans seem to be the one exception which have continued to outperform other classes of mortgage debt.

At the end of Q3 2023, 525 banks reported that they held commercial REOs, fewer than the previous two quarters.

Moving into Q4 2023 non-performing loans held by banks included:

- $1.4B in 30-89 day late owner occupied loans

- $15B in nonaccrual stage non-owner occupied CRE loans (up almost 30%)

- $2.5B in 30-89 day late non-owner occupied loans

- $3.4B in nonaccrual stage owner occupied CRE loans

The largest pool of non-performing loans is in nonaccrual stage non-owner occupied loans which rose around 30% in Q3 after a 25% jump between Q1 and Q2.

Find out which banks have the most non-performing commercial loans inside BankProspector.

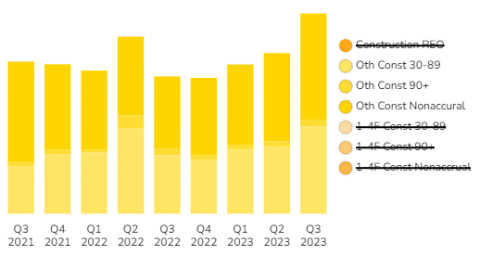

Construction Debt

Construction loan debt performance has deteriorated dramatically as well.

The largest percentage of this debt remains among commercial development loans with most defaults now in the nonaccrual stage. At almost $2B, this is a 20% increase from Q2 and up more than 30% compared to the same quarter last year.

This is followed by newly defaulting loans in the 30-89 day late stage, a pool of over $1.6B in loans. This is up from just $1.2B in Q2.

Banks are still holding just under half a billion dollars in construction REO, with 369 banks now reporting holding these non-performing assets. This suggests even more consolidation with fewer institutions holding this non-performing debt.

Other Debt

Agricultural

Farmland debt has continued to outperform all others over the past two years. Although performance is still near a two-year best, there was a small uptick in distress in Q3.

The largest part of this pool is around $673M in non-accrual debt followed by $321M in newly late loans, and just $55M in REO.

Business Debt

Business debt performance improved slightly from Q2.

More than $12B in nonperfoming C&I loans are in the nonaccrual stage. Newly late loans total around $6.7B. $2.6B sits in the 90 day plus category.

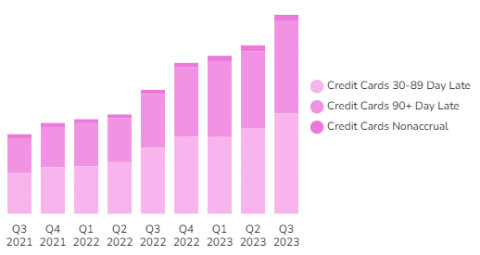

Consumer Debt: Auto Loans & Credit Cards

Both auto loan and credit card debt have continued their two-year climb to worsening performance. Both appear to have hit new highs of distress in Q3 2023.

No amount of bullish predictions in the media appear able to trump the real fundamentals in the economy that businesses and entrepreneurs are facing.

Ongoing hyperinflation, high taxation, rising interest rates, and tens of millions of jobs being wiped out by AI are still not likely to help create any change here over the next couple of quarters.

Around $12.6B in auto loans have recently fallen into default, up by around $1B from the previous quarter. Over $32B in credit card debt is now classified as nonperforming, a spike of around $5B from the previous quarter.

Looking Ahead

Commercial debt performance continues to deteriorate.

Almost every sector is showing worsening performance, with some categories of default seeing dollar volume more than double this year.

The big questions are whether lenders and note holders will stop the damage earlier this time, or not as well as how investors can cherry-pick the great deals from these pools.

What seems to stand out most is that while lenders hold little in the way of REOs, they do not appear to be curing performance issues before they fall into the nonaccrual stage. This could indicate substantial opportunity for investors to acquire these debt investments at a discount and do a better job at working with borrowers to create more value and cash flow.

Log in now to see which banks are holding the most distressed notes.