While the overall pool of non-performing residential mortgage loans stayed relatively flat from Q2, banks are dealing with more than $15B in 30-89 day late loans from Q3.

In spite of deteriorating debt performance in the multifamily, commercial, and credit card spaces, residential loans appear to be faring better. Although there remain tens of billions of dollars in opportunities for investors.

Let’s dive into the latest bank data from Q2 to see exactly what is going on…

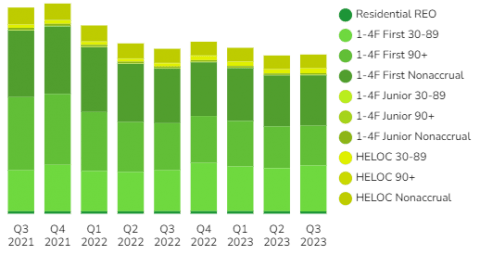

Banks Hold Over $44B in First Position Non-Performing Residential Mortgages

As in Q2, banks reported over $15B in first mortgages on 1-4 family properties which are in the 30-89 day late stage. That’s up by around $1B from the previous quarter, and up $5B from Q1, suggesting that more homeowners are trickling into financial distress.

Already ahead of those are around $16.5B first position nonaccrual loans on 1-4 family residences as well as almost $13B in 90 day plus late loans, which have not been classified as nonaccrual yet.

Residential REOs

656 banks reported that they held residential REO at the end of the third quarter of this year, up slightly from Q2.

At $747M, this is still a very small percentage of the total volume of distressed residential loans being held by banks right now.

This could accelerate as AI continues to eat more jobs, while fund manager Ken Griffin predicts high inflation could rage for decades, and more households wrestle with food insecurity due to sky-high grocery prices.

Non-Performing Residential Loans

The largest percentage of non-performing residential mortgage loans remains in the nonaccrual stage, with newly late loans right behind that.

As of Q3 the breakdown of non-performing first mortgage liens being reported includes:

- $15B in 30-89 day late loans

- $13B in 90 day plus late and still accruing loans

- $16.5B in nonaccrual loans

Discover the 3,000 plus banks holding these non-performing loans inside BankProspector now.

Junior Liens

At the end of Q3 2023 there were over $4.4B in nonaccrual stage revolving lines of credit. Additionally, there were around $1.5B in delinquent HELOCs behind those. The majority of which are newly defaulting lines of credit.

Defaults on revolving credit lines (HELOCs) continue to be many times higher than on fixed second mortgages.

Dive into the BankProspector dashboard to find out which banks are reporting the most distressed residential junior lien loans and HELOCS.

Looking Ahead

Bank data from the third quarter shows the residential loan market in about the same shape as Q2. While appearing healthier than other debt sectors, comparing the historical data shows we are experiencing a shift towards more serious defaults.

How this plays out will greatly depend on whether banks are able and willing to work with their borrowers to cure and stave off more serious defaults, a dynamic that seems unlikely to have a happy ending for many.

Even more impactful is the ongoing blitz of financial challenges impacting homeowners and home buyers.

Deteriorating consumer credit data suggest that more distress is coming.

This is a fantastic opportunity for investors to once again step in to seize on valuable opportunities, while saving many borrowers, banks, and the economy from the worst.

Log in now to see which banks are currently holding the most distressed notes…