Making Money in a Housing Market Crash (2021)

Coronavirus has changed everything and what’s in store next for the housing market is anyone’s guess.

But with soaring unemployment, stubbornly high forbearance rates, eviction moratoria and the like we can be certain that we’re in for quite a year.

I wrote not long ago that I suspect that the housing recovery is a farce.

It’s not my intention to be a wet blanket on a newly smoldering housing market. In fact, I’m hearing from a lot of listing agents that happy days are here again and its the best spring real estate market they’ve seen in years.

I do not doubt any of this.

What I do doubt is the sustainability of the price recovery. I mentioned my reasons in a previous post.

Well, lest ye think me some kind of crazy-nay-saying-curmudgeon poo-pooing “the recovery” for his own gains… be advised that Fitch, a well respected ratings agency, is blowing the same horn for the same reasons – I guess they finally read my post ;).

“While rising prices and sales volumes suggest a recovery, they are not moving in sync with key economic indicators that would otherwise support a sustainable price level,” Fitch stated in its most recent quarterly report [source:DSNEWS].

I recognize that simply calling BS on a real housing recovery isn’t all that constructive to someone looking for guidance on how to make money. So let’s talk about that.

How to Profit During this Mini Housing Bubble

- SELLERS, SELL NOW: If you own property that you’ve wanted to sell for a while but you’re waiting for the market to come back SELL IT NOW. Do not wait. This market, right now, is the opportunity to get the best pricing you’ve seen and that you’ll see for a while. This could change on a dime. Maybe you’ve got the spring, maybe you’ve got through the fall, I seriously doubt you’ve got much longer than that. The numbers just don’t jive – this won’t last.

- BANKERS I’M TALKING TO YOU “SELL NOW”. You’ve been looking for a ray of sun through the clouds. It’s here. Don’t look a gift horse in the mouth. Today is the day to take the loss that you’ve been putting off. If you miss this window you’ll be kicking yourself in 18 months. You’ve taken some write-downs, sell it now. Today is the best day that you’ve had in 4 years to mitigate your losses. Sell right now.

- BROKERS: Get thee to the “sell side” of the transaction. Its all well and good that you’re working with X number of buyers who want to pay 15 cents on the dollar and they have XX millions to invest. Great. But if everything you’re putting in front of your buyers is “priced too high” then you need to change your game because make no mistake, buyers are buying… just maybe not yours. A good buyers list is a fantastic resource, I’m not saying ditch it, but you should leverage your buyer’s list to find your seller clients. For every degree of separation, there is between you and the seller your chance of making a fee drops exponentially. Focus on how you can get sellers the most money in the least amount of time in this market – and prove it. When things turn again and buyers rule the day, and I believe it will, you’ll still have your relationships your sellers will need you more than ever and your picky buyers will still have capital and be ready to go.

- Buy and Hold – with cheap long term debt. I wouldn’t buy anything today that I planned to exit from in fewer than 5 years at an absolute minimum, 10-20 even better. Yes, interest rates are very attractive and go a long way to making numbers work and so that’s exactly how I would approach a purchase today, as a long term hold. If you’re thinking you’re going to snap something up and turn it over in 18 – 24 months riding nice annual 10% gains – I think you are nuts. The short term outlook is unknown, the fever pitch around recovery right now is driving false pricing. Buy for cash flow. Long term low cost debt is providing a real opportunity to see cash flow in places you never would have found it before. Don’t buy for appreciation and for goodness sakes don’t get into something today that you think you’re going to fix and flip unless you’re operating an organized disciplined flipping machine and you know for a fact you will get out before the holidays.

- Investors – buy the debt. When you hold the debt position (the loan, the mortgage, the note, the trust deed) LTV cures all ailments. If you’re looking for something to invest in today sure, you can buy real estate and take on the debt, the other side of it is to buy the debt and be the bank. Why? Because it is a much more secure position when future values are in question. Consider this math: Imagine you have $100,000 to invest. You can use this as a downpayment for a $400K investment and borrow $300k. What happens if the market slips 10% in the next 24 months. Well, on paper you are out $40k, you’ve lost 40%. Now turn that around. What if you invested your $100k as a first position lien on a property purchase on a 80/20. Someone buys a property for $125K, they bring $25K, you loan $100K (total purchase $125k). The market drops 10%… the owner is down 50% ($25K – $12.5K) and as the lender, you have lost nothing. Obviously, this is a simple example… but I hope you get the point.

Don’t get caught up in the hype. There are real opportunities out there but you have to be using your critic’s eye.

Warning Signs

If you’ve got a plan or a system that you’re working in this market we’d love to hear about it in the comments below. If you’re looking to do more note and REO deal directly with lenders – check this out.

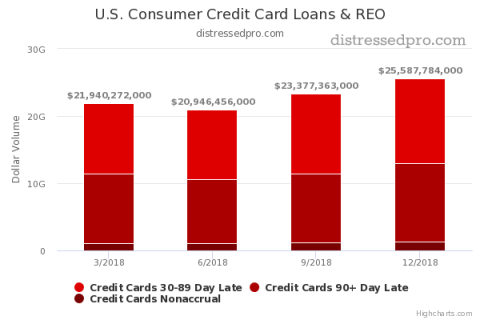

We’re seeing a 9.5% increase in consumer credit cards from $23.3 Billion to $25.5 Billion

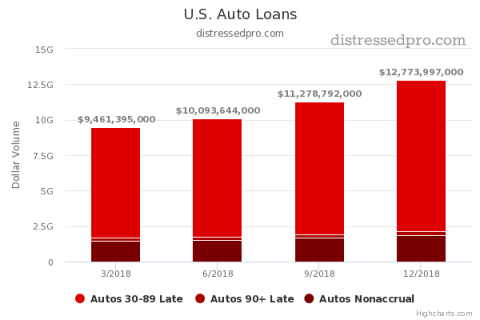

and an increase of 13.3% in auto loan defaults from $11.2 Billion to $12.7 Billion

These are signs of stressed consumers.

Credit cards and auto loans are the first things to go when people start to tighten their belts and with the stock market due for a correction, we are looking at a perfect storm for another crash in the housing market.

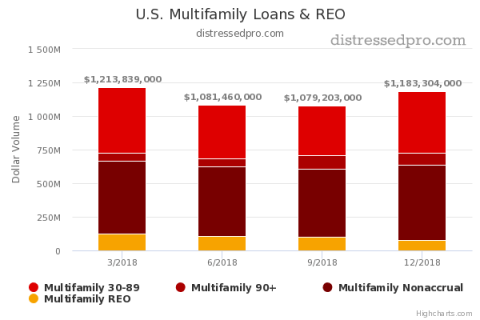

We are already seeing the signs in multifamily which has increased by 9.6% after more than 5 years of decline.

- Explain what these increases meant before the last crash

These are all signs of increased consumer pressure, credit card, and auto loans have always served as the “canary in the coal mine” for the housing market.

We expect to see increased defaults in coming quarters in residential mortgages.

Housing crash timeline

January 2017 – 30 Charts Proving We’re In The Mother of All Financial Bubbles

April 2017 – The Car-Loan Boom isn’t the Housing Bubble. But there still might be a Crash

January 2018 – Another Housing Bubble Could be Ready to Erupt

September 2018 – JP Morgan’s Top Quant Warns Next Crisis to have Flash Crashes and Social Unrest not Seen in 50 Years

November 2018 – Dallas and West Coast Ground Zero for Next Housing Bust

January 2019 – Housing Bear Who Called 2018 Slowdown Says Worst Yet to Come

Notes VS Property

My experience holding property in 2008

In 2008 I was neck deep in real estate. I had a condo project in the works and I owned a real estate brokerage. I had 100% of my assets and income invested in or coming from real estate. I can tell you from personal experience that being fully invested in real estate during the housing market crash can be a horror show. If I knew then what I know now, I would have still been invested in real estate however, I would’ve done it quite a bit differently.

You see I was invested in real estate as the owner. That means that my interest was at the very tippy-top of the capital stack. When things go bad in real estate the last place you want to be is at the top of the capital stack.

As the market turned and my business turned into foreclosures and note sales instead of investment sales and flips, I came to learn the power of being invested in the debt rather than being invested as the equity.

How owning notes is better

When you own the debt especially the first position debt in your property, your interest in that property should be well covered by the collateral. What that means is that in a downturn or housing crash, when you’re invested in the debt instead of the equity, the equity gets wiped out first and the owner of the debt becomes the winner.

How to start investing in notes today

The fastest way for you get started investing in the debt side of real estate rather than the equity side is by finding notes for sale. Finding the notes is the very first step in becoming a note investor.

If you have more capital to invest then you do time, then you should try to partner with people who are in the business of finding notes so that you can get invested. If you’re like most people and you have a little more time than capital to invest, then you should get started looking for notes.

The easiest way to do that is with BankProspector.