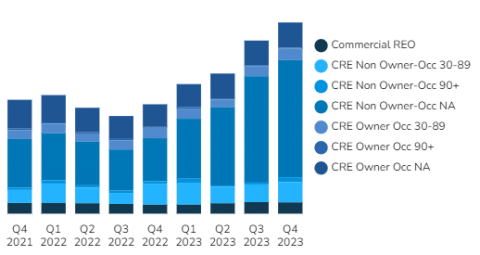

Commercial loans set another new record for non-performing volumes in Q4 2023. Yet, again, marking another two-year high in delinquency and distress.

CRE mortgage debt, as well as consumer debt has seen distress escalating in an epically dramatic way this year.

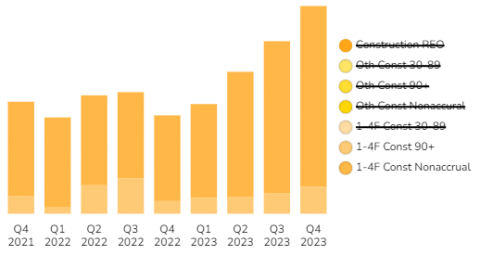

The two exceptions this quarter appeared to be construction loans, and once again, farmland loans, which have continued to outperform other classes of mortgage debt.

At the end of Q4 2023, 517 banks reported that they held commercial REOs, a rate that had been declining all year.

Moving into Q1 2024 non-performing loans held by banks included:

- $1.6B in 30-89 day late owner occupied loans

- $16.4B in nonaccrual stage non-owner occupied CRE loans

- $2.8B in 30-89 day late non-owner occupied loans

- $700M in 90+ day late non-owner occupied loans (A 175% volume increase from the previous quarter)

Find out which banks have the most non-performing commercial loans inside BankProspector.

Construction Debt

Non-performing construction loan volume remains near its recent highs.

The largest percentage of this debt remains among single-family and twinhome development loans, with most defaults now in the nonaccrual stage. At $3.3B, this is up substantially from the previous 3 quarters, and has increased in volume by 90% since Q1.

This is followed by newly defaulting loans in the 30-89 day late stage; a pool of over $1.2B in loans, back down to similar levels seen in Q2.

Banks are still holding just under half a billion dollars in construction REO, with 359 banks now reporting holding these nonperforming assets.

It is worth noting that more developers appear to be selling off whole projects, which may help pay off loans. Though indicates a pessimistic outlook of the new homes sales market.

Other Debt

Agricultural

Farmland debt has continued to outperform all other debt classes over the past two years, which may have been further aided by the recent and ongoing boom in the cannabis industry.

The largest part of this pool is around $650M in non-accrual debt, followed by $340M in newly late loans, and just $59M in REO.

Business Debt

Business debt performance has deteriorated again, now close to its two year record high for delinquency and defaults.

More than $13B in nonperfoming C&I loans are in the nonaccrual stage, which is up $1B over the previous three months. Newly late loans total around $8B, up by $1.3B. And, $2.8B sits in the 90 day plus category.

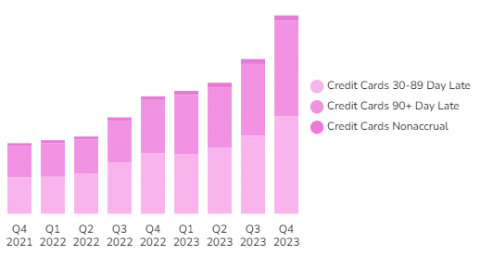

Consumer Debt: Auto Loans & Credit Cards

Both auto loan and credit card debt have continued their two-year streak of worsening performance, hitting dramatic new highs of distress.

The question remains just how much these debt pools can balloon before they impact the wider economy.

Ongoing hyperinflation, high taxation, rising interest rates, and tens of millions of jobs being wiped out by AI are still not likely to help create any change here over the next couple of quarters.

Around over $20.5B in credit card debts have recently fallen into default. Another $20B is over 90+ days late. Over $17B in auto loan debt is now classified as nonperforming.

Looking Ahead

While we are seeing some moderation in construction debt performance, and farmland loans continue to do well, overall commercial debt performance continues to deteriorate, with dramatic volumes of defaults among credit cards and auto loans.

Few mortgage defaults seem to be ending up sitting on lenders’ books as REO, suggesting an appetite for well-priced deals, with plenty of opportunity for conversions and repurposing property in booming industries.

The data hints at a widening disparity, with masses in financial trouble, and some big winners that seem to be snowballing their gains.

Log in now to see which banks are holding the most distressed notes.