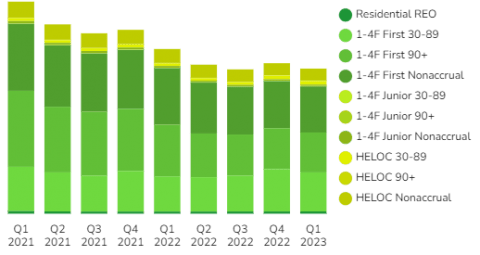

Distressed residential mortgage loan performance saw minimal improvement or decline in Q1 2023, with figures nearly identical to the previous quarter’s data.

Small declines in almost all stages of distress leave this pool split almost evenly between the main categories of newly late, 90 day plus late loans, and nonaccrual mortgage loans.

Junior liens continue to show signs of mounting distress, with a slight uptick in distressed HELOC loans tumbling into the 90+ nonaccrual stage.

Let’s dive into the latest bank data to see exactly what is going on…

Banks Hold Around $48B First Position Non-Performing Residential Mortgages

There are currently just over $14.6B in first mortgages on 1-4 family properties which are in the 30-89 day late stage; this is slightly less than the previous quarter’s $15.8B.

Already ahead of those are around $17.2B first position non accrual loans on 1-4 family residences as well as nearly $15B in 90 day plus late loans, which have not been classified as non accrual yet.

Residential REOs

Banks reported that they held a combined $840M in residential REO at the end of the first quarter of this year, up from $830M in Q4 2022.

This is still a small portion of the total volume of distressed residential debt being held by banks but an important data point to watch. At the point that non-performing assets are not being absorbed by the market, banks can find themselves in more trouble.

Ongoing high inflation, soaring interest rates, a drop in home sales activity, and declining home prices, along with rising unemployment, all seem likely to drive more home loan defaults and foreclosures this year.

Non-Performing Residential Loans

The largest percentage of non-performing residential mortgage loans are non-accrual stage.

As of Q1 the breakdown of non-performing first mortgage liens being reported includes:

- $14.6B in 30-89 day late loans

- $14.9B in 90 day plus late and still accruing loans

- $17.2B in non-accrual loans

Discover the 3,000 plus banks holding these non-performing loans inside BankProspector now.

Junior Liens

At the end of Q4 2022 there were over $5B in total nonaccrual stage junior liens and revolving lines of credit. Q1 2023 saw minimal improvement, with figures still totaling around $5B.

Defaults on revolving credit lines (HELOCs) continue to creep up, though fixed second mortgage liens saw a small drop in distress.

Dive into the BankProspector dashboard to find out which banks are reporting the most distressed residential junior lien loans and HELOCS.

Looking Ahead

Bank data from Q1 2023 shows the distressed residential loan market in a gridlock, with minimal change from the previous quarter.

It may come as no surprise to some monitoring the broader economic scope. As banks and borrowers face evolving lending and market conditions, the wide barrage of financial challenges impacting homeowners and home buyers certainly isn’t over yet.

If there are not major shifts in monetary policy, employment, and the overall economy, it is likely more distress will come. For now, there are still very few REOs. That could change if house prices continue to decline, and buyers remain on the sidelines.

Some have predicted that the worst of the housing downturn is over, while more investors may be waiting on the sidelines for better priced deals as market conditions decline.

Log in now to see which banks are currently holding the most distressed residential notes…