![U.S. Commercial Loans and REO Chart - Historical [Q4 2021]](https://www.distressedpro.com/wp-content/uploads/2023/02/U.S.-Banks-Commercial-Two-Year-Historical-Q4-2022.png)

Non-performing commercial mortgage loans appear to have reversed course, with increasing levels of distress. This reversal of the trend we’ve seen for the past two years also mimics what was reported in the multifamily and residential sector in Q4 2021.Â

Farmland loans appear to be the one exception to these negative trends in the real estate debt space.

Most notably among commercial loans in the fourth quarter were increases in newly late non-owner occupied loans, as well as non accrual stage non-owner occupied loans.

As of the end of Q4 2022, 571 banks reported that they held commercial REOs, representing a small decline in commercial REO value and the number of banks with them on their books.Â

Even the largest corporations have been consolidating space, with Twitter notably being hit with a lawsuit for failing to even pay rent on its HQ. The world’s largest fund, Blackrock was recently in the headlines for blocking investor withdrawals from one of its property funds, suggesting that liquidity has become a problem for even the biggest and most global institutions. It’s worth noting that a Blackrock failure would be many times larger than FTX and Lehman Brothers.

Moving into Q1 2023 non-performing loans held by banks included:

- $1.5B in 30-89 day late owner occupied loans

- $6B in nonaccrual stage non-owner occupied CRE loans

- $2.9B in 30-89 day late non-owner occupied loans (almost double the previous quarter)

- $3.1B in nonaccrual stage owner occupied CRE loans

Note there are around $4.5B in newly defaulting loans in the 30-89 day late range.

Find out which banks have the most non-performing commercial loans inside BankProspector.

Construction Debt

![U.S. Construction Chart [Q4 2022]](https://www.distressedpro.com/wp-content/uploads/2023/02/U.S.-Banks-Construction-Historical-Q4-2022.png)

Construction loan debt performance appears to have stayed flat on a total volume basis.

The main change in the past quarter appears to have been more late loans falling into the nonaccrual stage.Â

This follows a significant spike in defaults in Q2 2022, during which the market erased all improvements from the previous year.

Banks are still sitting on just under half a billion dollars in construction REO with 420 banks now reporting holding these nonperforming assets.Â

The largest percentage of this debt is in commercial development and land acquisition loans, which are now in the nonaccrual stage. This seems to suggest that borrowers that fell into default throughout 2022 were unable to catch up on their loans or cure them.Â

Extreme inflation, never ending crises, the end of the traditional office, recessionary indicators, and diving home prices may be at play here.

Other Debt

Agricultural

Farmland debt seems to be the clear best performer in Q4 data.

Continuing its positive run in getting healthier for the past two years, farmland is the only sector that hasn’t fallen negative this quarter.Â

The largest part of this pool is around $700M in non-accrual debt followed by $292M in newly late loans, and just $64M in REO.Â

Business / C&I Debt

Business debt performance is still in worse shape than in Q2 2022, though shows marginal improvement from Q3 2022.Â

More than $1B non-performing C&I loans appear to have rolled over into the 90 day plus late stage with almost $10B in the nonaccrual stage.Â

Behind that is another almost $9B in 30-89 day late loans.

With countless challenges facing businesses of all sizes today, it shouldn’t be surprising if we see more distress coming in this sector as well as fewer new business loans being originated.

Consumer Debt: Auto Loans & Credit Cards

![U.S. Auto Loans Chart [Q4 2022]](https://www.distressedpro.com/wp-content/uploads/2023/02/U.S.-Banks-Auto-Loans-Historical-Q4-2022.png)

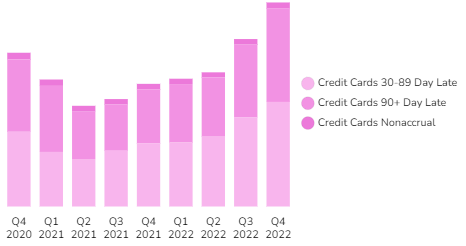

Both auto loan and credit card debt continue to see steep trajectories in failing performance. This has continued to balloon since early 2021.Â

Borrowers have fallen late on around $2B more in credit card debt in the last three months of 2022, pushing total distressed credit card and auto loan debt in Q4 to the highest levels in two years.

Over $12B in auto loans were 30-89 days late in Q4 2022 as well.Â

Consumers normally don’t bounce back on track in January after the holidays. It may be possible that some will be able to get caught up with their annual tax refund money.Â

Looking Ahead

Commercial mortgage loan performance once again reversed course, following trends in multifamily and residential mortgage debt.

Auto loan and credit card debt has continued to deteriorate in performance over the past two years, with even more falling behind on their payments in the past three months. It’s a steep upward curve that doesn’t seem to have a positive ending for consumers.Â

The real star performer from a lender’s perspective remains agricultural and farmland debt.

Log in now to see which banks are holding the most distressed notes.