The total volume of commercial mortgage loan defaults appears to have hit the lowest points since the beginning of the COVID pandemic.

Banks are reporting a modest decrease in distressed CRE loans for the end of Q2 2022, reversing the direction of the market we saw in Q1 of this year.

![U.S. Commercial Loans & REO Chart - Current [Q2 2022]](https://www.distressedpro.com/wp-content/uploads/2022/08/commercial-current-q2-2022.png)

Commercial REO

The one big difference in this sector from other categories of mortgages is there being more commercial REOs ($1.4B) than residential and multifamily combined.

At the end of Q2 2022, 679 banks reported holding commercial REOs, a further decline from Q1 this year and the second half of last year. It appears fewer banks are exposed to this risk today than in 2021.

Commercial Real Estate Loans

The majority of distress still remains among non-owner occupied CRE loans in the non-accrual stage, making up 41% of all distressed CRE mortgage loans.

Office and retail properties and, more recently, industrial real estate have all had challenges over the past couple of years.

The improvements in this data could suggest that tenant companies have been adjusting well to economic changes while those serving the new economy, such as tech startups and biotech companies, have been growing and adding more space.

Moving into Q3 2022, non-performing loans held by banks included:

- $1.1B in 30-89 day late owner-occupied loans

- $6.1B in non-accrual stage non-owner occupied CRE loans

- $2.2B in 30-89 day late non-owner occupied loans

- $3.4B in non-accrual stage owner-occupied CRE loans

All of these categories have seen declines in volume over the past quarter.

Note there are around $3.3B in newly defaulting loans in the 30-89 day late range.

Find out which banks have the most non-performing commercial loans inside BankProspector.

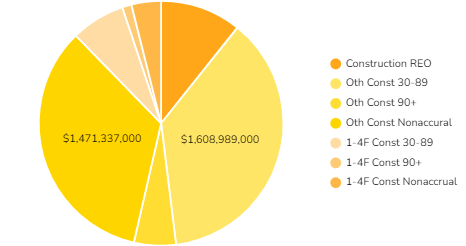

Construction Debt

Construction debt has seen one of the most significant spikes in distress among real estate loans. New data shows the market reversing and erasing all improvements from the previous year.

Banks are still sitting on around half a billion dollars in construction REO, just under the level of residential REO; 475 banks report holding these properties.

The largest percentage of this debt is among commercial development and land acquisition loans that are 30-89 days late. This pool is now over $1.6B, an increase from the previous quarter.

Extreme inflation, supply chain issues, never-ending crises, slowing price growth, and the potential for an oversupply of new construction may be at play here.

Other Debt

Agricultural

Farmland loan performance seems to be the healthiest under the CRE umbrella this quarter. It is the only sector that hasn’t seen an increase in distress.

This trend line shows steady improvement since the beginning of 2021.

The largest part of this pool is $900M in non-accrual debt, followed by $286M in newly late loans and just $69M in REO.

Business / C&I Debt

We’ve seen non-performing business debt levels elevated since the second half of 2021. This quarter’s most significant increase has been in the non-accrual stage, which has risen by around 30%, following a similar trend in 90+ day late loans last quarter.

This suggests that some business owners have just given up paying or have gone bankrupt.

Investors looking for a big market to take on will find there are almost $10B in non-accrual stage loans in this category as of the end of Q2 2022.

There were over $12B in late C&I loans coming behind that as well.

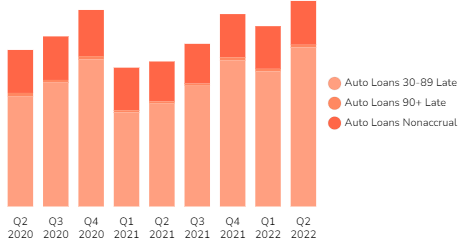

Consumer Debt: Auto Loans & Credit Cards

Auto loan performance seems to have continued to deteriorate since the beginning of 2021. This seems to squash any hope that Q1 data was simply a seasonal blip and transitory. As predicted last quarter, we are now seeing an all new two-year high in distressed auto loans.

77% of this pool of distressed debt is new 30-89 day late loans totaling over $9B, up about $1.5B from Q1 2022 and almost $4B from the previous year.

Gas prices may certainly be a factor in this, one which won’t change until we see much more dramatic drops in energy prices.

Credit card performance also continued to deteriorate over the last year, completing a full year of rising distress in this market. Over $16B of debt sits in this pool.

Consumers appear to be maxed out, with many businesses suffering from their lack of disposable spending cash. While it hasn’t yet, following revolving debt and car loan defaults, mortgage performance is likely the next to feel the impact unless these trends are reversed quickly.

Looking Ahead

Commercial mortgage loan performance actually appears to be surprisingly strong, given all the negativity about the economy in the media.

However, with the exception of farmland loans which are performing well, all other areas have continued to deteriorate, including business and auto loans and credit card debt.

This waterfall effect is expected to eventually hit the mortgage market. Until now, stimulus and fast-rising house prices effectively put a dam in place to prevent this. If those things fall apart, the impact could be felt by banks and lenders much faster than some anticipate.

Log in now to see which banks are holding the most distressed notes.